About Risk

What is risk? Most of us think about potential losses when we think about risk. We focus on the consequences of risk, and particularly the adverse consequences associated with the risk. However, the word "risk" is derived from the Latin word risicare, which means "to dare." The word risk implies choice. After all, it is the potential reward associated with a risk that attracts the entrepreneur to dare to engage in a business venture. And, based on the plethora of risks they face, farmers must be daredevils. We should not associate risk with bad luck or victimization. Like rolling dice, the probability of rolling a seven or eleven is exactly the same every time you role. It is why the casino always wins, eventually. Risk may be unavoidable for the farmer, but it is manageable.

What is risk? Most of us think about potential losses when we think about risk. We focus on the consequences of risk, and particularly the adverse consequences associated with the risk. However, the word "risk" is derived from the Latin word risicare, which means "to dare." The word risk implies choice. After all, it is the potential reward associated with a risk that attracts the entrepreneur to dare to engage in a business venture. And, based on the plethora of risks they face, farmers must be daredevils. We should not associate risk with bad luck or victimization. Like rolling dice, the probability of rolling a seven or eleven is exactly the same every time you role. It is why the casino always wins, eventually. Risk may be unavoidable for the farmer, but it is manageable.

The Farmer Faces Many Types of Risk

• Production Risk (variations in weather, disease, insects, bad seed, etc.)

• Price Risk (Fluctuations in input costs/sale prices, poor hedging, timing, etc.)

• Casualty Risk (Fire, flood, windstorms, theft, etc.)

• Uncertainty Risk (Lease terms/rent, borrowing costs, government programs, etc.)

• Legal Risk (lawsuits, water rights, partnerships, etc.)

• Labor Risk (Sickness, injury, losing a "key" person, etc.)

• Technological Risk (Equipment failure, technological obsolescence, etc.)

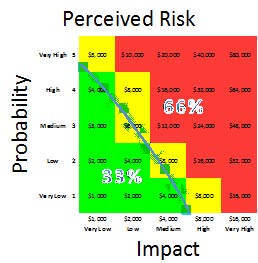

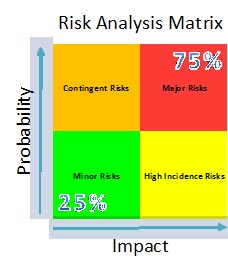

Quantifying risks is as important to the farmer's enterprise as identifying risks, because it assists in prioritizing risks and identifying decisions to be made. There are two elements which need to be quantified before any assessment can be made about the cost and economics associated with reliably controlling risk. These are: 1) the probability of the risk occurring, and 2) the impact and economic consequences of it occurring.

Quantification of risk is fundamental to any business decision. Unfortunately, many farmers do not properly analyze their risk or simply do not have sufficient capital available to cover the risks associated with the failure of key farm machinery. They just hope they are lucky enough to not roll "craps" and somehow get through another season without a catastrophic failure. When they are not lucky, they must deplete their profit/reserves, turn to expensive financiers to cover repairs or they may go broke.

There are three basic ways to manage risk:

1) Absorb Risk:

This is appropriate when capital is sufficient to withstand an occurrence without excessive impact to cash flow or reserves. If the enterprise is absorbing many risks, the possibility of a number of issues occurring at the same time should be considered. Therefore, the capital reserves behind a farming enterprise should be sufficient to withstand the occurrence and financial consequences of most risks. Typical risks are the normal fluctuations in market prices of products, changes in international currency rates, increases in labor costs, increases in the price of feed due to shortages or the breakdown of machinery. Absorbing risks requires positive action and not simply acceptance that the enterprise can withstand the loss should it occur. This alternative requires maintaining a certain level of financial liquidity by reserving a fixed percentage of profits or strict regard to specific practices that reserve capital in what some call a "rainy day fund." However, in farming a better name might be: It didn't rain fund.

2) Avoid Risk:

For equipment, this is things like preventative maintenance, buying reliable machinery with sufficient power to handle your tasks, and trading-in equipment while it is still covered by a service contract. Risk is avoided, for instance, when a farmer chooses not to plant a crop that is susceptible to drought when they expect a dry season, or not using a machine for an application for which it is not intended.

3) Transfer Risk:

Transfers of risk occur when one party lowers their risk by shifting that risk to someone else. There are numerous methods in agricultural production to shift risks, for example: futures and options contracts, crop insurance, fire and hail insurance and buying extended service contracts on machinery. These transfers are accomplished with a known cost, i.e. the cost of the extended service contract.

Obviously, risk and uncertainty cannot be totally eliminated. In fact, doing so could result in the elimination of the chance for any profit, since by definition one of the components of profit is a reward for risk-taking. However, some risks can be reduced to acceptable levels without significantly reducing the opportunity for profit.

Insurance is a common method used to reduce the financial consequences of adverse events. The fundamental principle of insurance is to pay a premium for someone else to take the risk. Insurance programs are commonly used to manage other risks on the farm like: health and medical risk, casualty risk, accident risk, liability risk, weather risk, etc. For most major commodity crops, crop insurance is available to reduce the risk exposures due to price and yield variability. An extended service contract offers the same kind of protection and should be considered as an essential way to transfer the risk of machinery failure for a reasonable expense.